On March 1, 2025, two important Circulars from the State Bank of Vietnam (Circular 64/2024/TT-NHNN and Circular 50/2024/TT-NHNN) will officially take effect. This marks both an opportunity and a new challenge for banks, financial institutions, and API/APIM solution providers.

Circular No. 50/2024/TT-NHNN, dated October 31, 2024, stipulates safety and security for providing online services in the banking sector, detailing the assurance of safety and security in online banking infrastructure, electronic transaction verification, and operational management.

Meanwhile, Circular No. 64/2024/TT-NHNN regulates the implementation of open application programming interfaces in the banking sector, clearly outlining the rights and responsibilities of banks, third parties, implementation principles, the Open API catalog, and detailed technical standards. These provisions are mandatory for all participating parties.

Open API is an important and highly applicable connection protocol that facilitates data sharing and the development of technology solutions, as well as the interaction process between systems. The process of connecting and sharing data based on APIs will help banks and partners create new solutions, products, and services that leverage the advantages and unique characteristics of each party’s ecosystem. Open API is a core component in building Open Banking and inclusive finance—a necessary development direction and the near future of global finance.

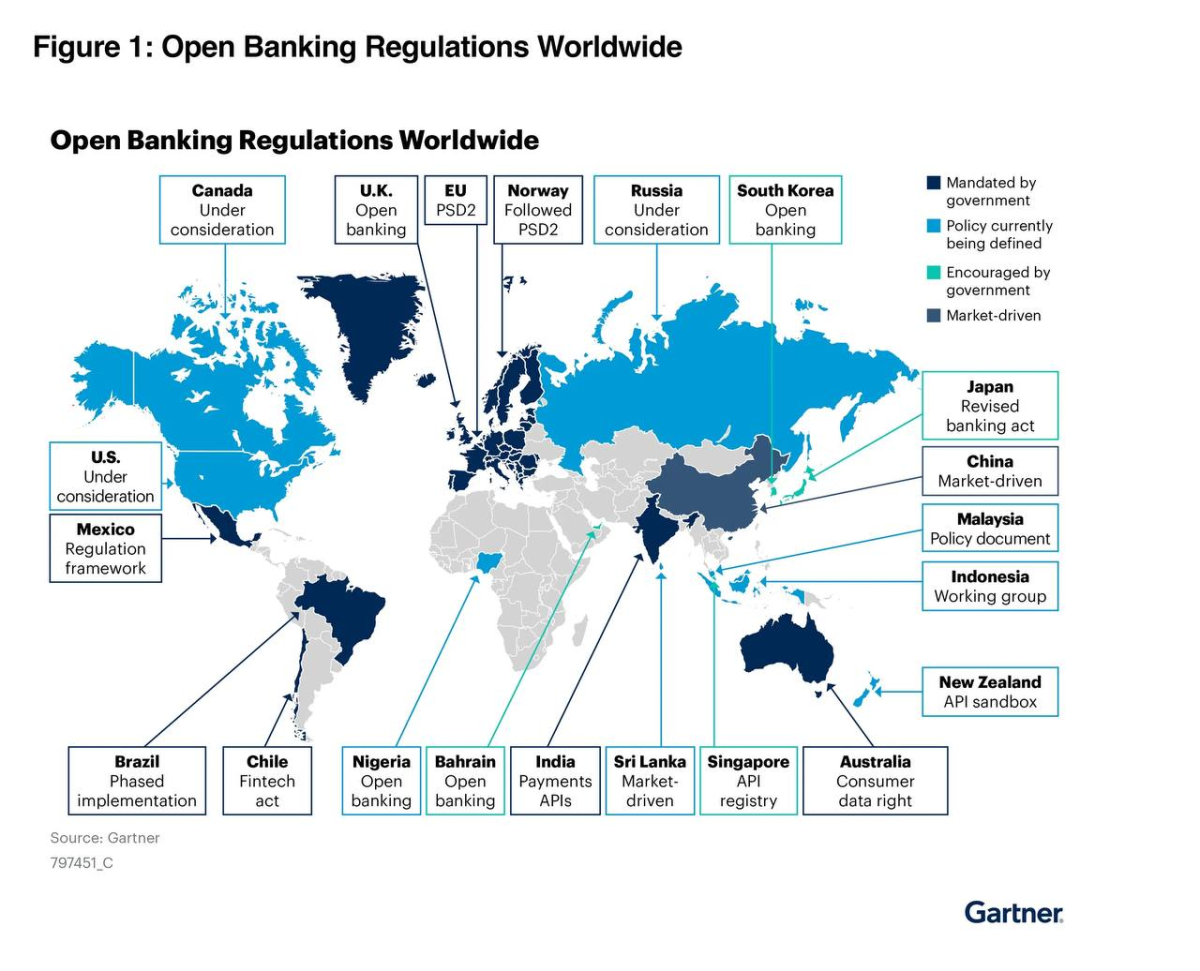

In Vietnam, prior to the regulations on data standards and Open API technical standards, many banks had proactively opened part of their data to third parties. The implementation of Open API is relatively common. As a latecomer, having only issued the Circular related to Open Banking on December 31, 2024 (Circular No. 64/2024/TT-NHNN), Vietnam has adopted advanced regulations from around the world regarding Regulation Framework, Open Banking API Specification, Data Security, Consent Regulation, Technical Specification, etc. Therefore, Vietnam’s legal documents are considered updated and integrated with international standards.

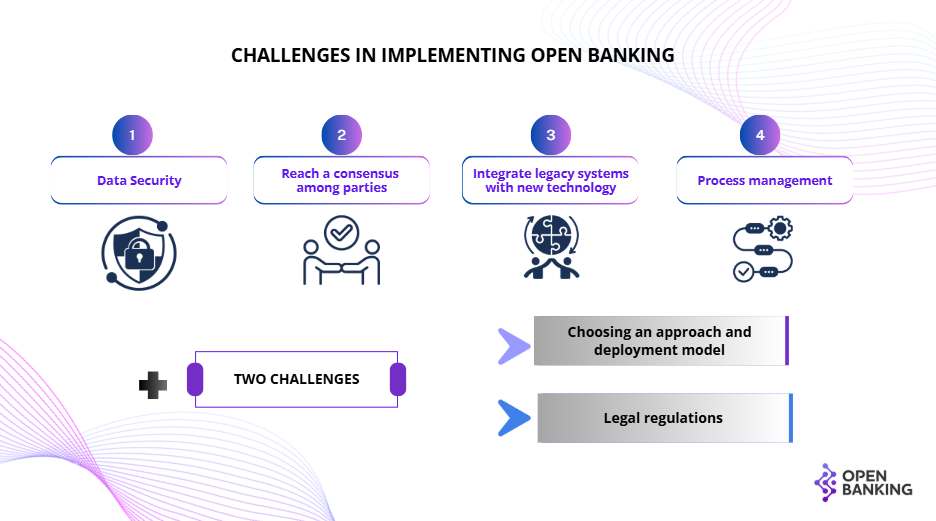

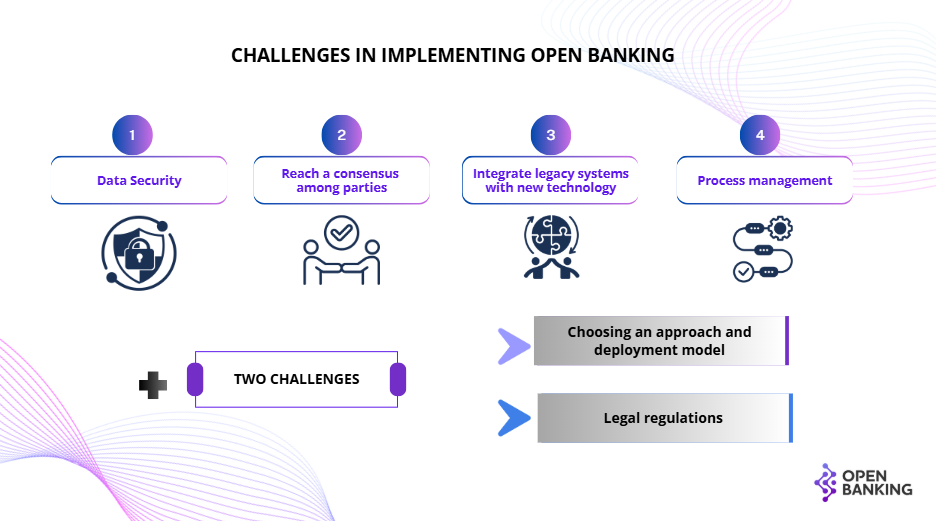

Developing Open Banking, alongside considerations of approach and implementation models, legal regulations, faces the biggest challenge of achieving consensus among participants, integrating legacy systems with new technologies, establishing operational processes, and especially ensuring data security (largely the risk of sharing data with third-party providers – TPPs through APIs).

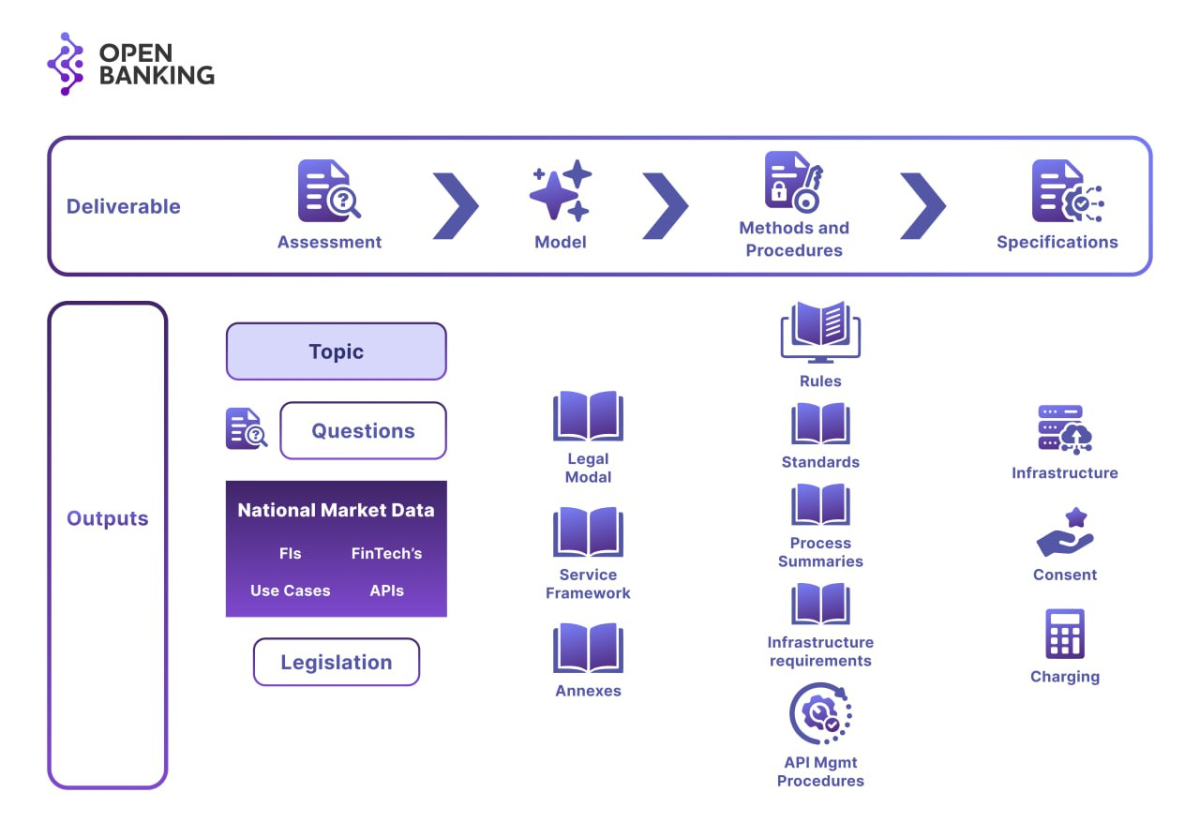

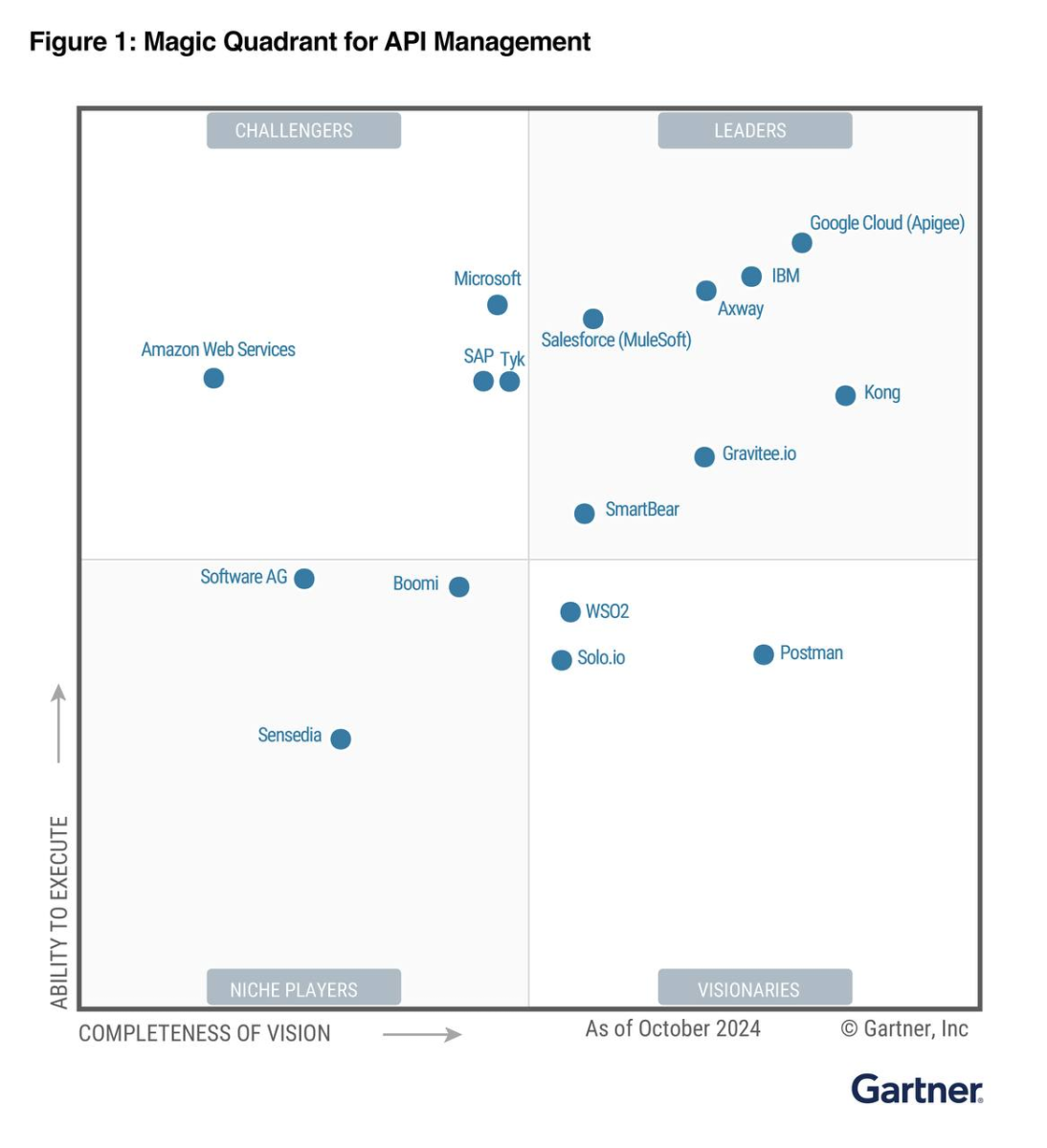

To truly harness the potential of Open Banking API/Open Banking Platform while ensuring data security, banks and financial institutions need to comprehensively assess the current state of infrastructure, technology, and governance processes, while also evaluating their ability to comply with Vietnamese legal regulations. Accordingly, participants should not only focus on procuring API Management components from technology companies like IBM, WSO2, Kong, Mulesoft, etc., but also on building and implementing other technical components and modules such as consent management modules, Strong Customer Authentication (SCA) modules, cybersecurity, data protection, etc., in accordance with the provisions of Circular 50/2024/TT-NHNN, the Cybersecurity Law, Decree 85/2016/ND-CP on ensuring information system security by level, the Electronic Transactions Law 2023, and Decree 137/2024/ND-CP on electronic transactions.

Gartner’s ranking assessment of API Management components—one of the key components of implementing the Open Banking Platform.

This presents both an opportunity and a challenge for banks, financial institutions, and Vietnamese technology partners in choosing or developing products and services that fully comply with legal regulations, easily integrate with reasonable operational and investment costs. Because more than anyone else, they understand the legal regulations and technical standards as well as the local culture to build appropriate solutions for the market. Reducing dependence on foreign API providers, lowering costs, shortening implementation time, and increasing the value of Make-in-Vietnam products and services in the Open Banking ecosystem are clear benefits if parties can seize this opportunity.

Steve Hoang – Deputy Director of Vietnam Innovation & Digital Transformation Institute